Need tax relief help? Learn about how the IRS collects back tax debt and what you can do to resolve it.

The IRS collections process

The IRS creates an account receivable when a taxpayer incurs tax debt. In order to collect from the taxpayer, the IRS then follows a series of steps.

The first step involves a series of computer-generated notices that are sent to the taxpayer. The taxpayer may contact the IRS at any time to make arrangements for the debt.

The first notice is a CP 14 Notice, which will look like this:

After the CP 14 Notice, the IRS automated system will continue to send notices every five weeks. The next notices will be a CP 501 notice, followed by a CP 503, and finally a CP 504.

If the taxes are not resolved during this initial phase, the case will be transferred to the Automated Collections System (ACS) or to a field revenue officer.

ACS works with taxpayers over the phone. Revenue officers will visit the taxpayer’s home or place of work.

While revenue officers sometimes do call taxpayers, they do not threaten lawsuits or criminal action. ACS does not initiate telephone contact.

If you owe payroll taxes, or owe over $250,000, the case will be transferred to a revenue officer. Otherwise, you will deal with ACS.

ACS enforcement

If the taxes remain unpaid after the automated notices, ACS will send a final Notice of Intent to Levy.

The final notice of intent to levy is very important. It the final notice required for the IRS to levy assets; they do cannot do so legally before this notice.

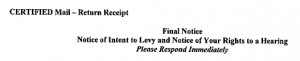

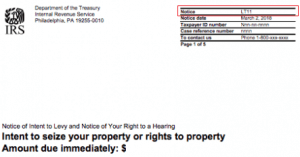

The CP 504 notice looks like a final notice of intent to levy, but it is not. The final notice will be either a Letter 1058 or LT11 and will look like the below.

Letter 1058:

Notice LT11:

If you receive either of these two notices, you or your representative need to contact the IRS within 30 days to make arrangements or to request a collections due process hearing.

After the 30 days to respond have lapsed, the IRS can levy your wages, self-employment income, and bank accounts. So it is important to not ignore this notice!

Revenue officers

Taxpayers who owe employment taxes or owe more than $250,000 will have a revenue officer assigned to their case.

Revenue officers are IRS civil enforcement employees who work cases that involve an amount owed by a taxpayer or a delinquent tax return. Their role involves education, investigation, and when necessary, appropriate enforcement.

Generally, home or business visits are unannounced because scheduling appointments for such matters would be inconsistent with their proactive and urgent nature. For example, many urgent and complex cases involve employers’ employment tax withholding requirement.

ROs carry two forms of official identification, a pocket commission and a HSPD-12 card. The HSPD-12 card is a government-wide standard form of identification for federal employees.

Both forms of identification have serial numbers and photos of the employee – and you can ask to see both. When at a home or place of business, the RO can also provide an additional method to verify their identification.

IRS Tax Debt Relief Programs

In order to qualify for a collection alternative, the IRS will require you to be current with your taxes. This means that:

- You’ve filed all of your tax returns that are due

- If you’re required to make estimated tax payments, you’ve made them for the current period.

If you’re current with your taxes, then you can request tax relief help (i.e., collections alternatives). There are several options available.

Short-Term and Long-Term Installment Agreements

The IRS has short-term and long-term payment plans available:

- Short-term payment plan: 6-month payment terms for balances of $100,000 or less.

- Streamlined Installment Agreements (SLIA): 72-month payment terms for balances of $50,000 or less.

- Non-streamlined installment agreements (NSIA): 84-month payment terms for balances of up to $250,000.

Partial Payment Installment Agreements

If because of your financial situation you’re not able to make the payments required under a streamlined or non-streamlined installment agreement, you can request a partial payment installment agreement (PPIA).

In order for the IRS to consider a PPIA, they will request financial information to determine if you qualify.

Currently not Collectible

If you’re not able to make any payments, the IRS will consider placing your account in currently not collectible (CNC). The IRS will place taxpayers into CNC status when their monthly allowable living expenses exceed their monthly income.

This is commonly used when a taxpayer temporarily unemployed. A CNC status is not permanent. When your financial situation changes, the IRS will reach back out to get you on a payment plan.

Offer in Compromise

In some cases the IRS will settle your tax debt through an Offer in Compromise (OICs). The IRS wants to get the most it can in a reasonable amount of time, and if that means settling the debt they will.

Most taxpayers are not good candidates for an offer in compromise. It is recommended that you work with a tax professional if you want to explore an offer in compromise.

Innocent Spouse Relief

When married taxpayers sign a joint return, they are jointly and severally liable for the taxes owed on the return.

Oftentimes a spouse will fail to report income or claim improper deductions or credits, without the other spouse knowing. In such cases, it might be grossly unfair to hold the innocent spouse liable for the other spouse’s mistakes.

The IRS provides three types of relief for such taxpayers: 1. Innocent spouse relief, 2. Separation of liability relief, and 3. Equitable relief.

Staying out of trouble after you’ve resolved your tax debt

If the IRS agrees to one of the tax relief programs discussed above, they will require you to remain in compliance going forward.

That means you must timely file your tax returns and must pay all new taxes as they are due.

You should look into making estimated tax payments and/or adjusting your W-4 so you don’t continue to owe taxes every year!