This article discusses what an IRS levy is and how to stop an IRS levy.

IRS levy vs. lien

A federal tax lien encumbers a taxpayer’s property. It is filed with the county clerk and is intended to provide notice to 3rd parties (such as creditors) that the IRS has a secured interest.

In almost all cases, the IRS will file a tax lien if the tax debt is over $10,000. If it’s less than $50,000, a lien can be prevented by entering into a streamlined installment agreement.

An IRS levy, on the other hand, is a legal seizure of property to satisfy federal tax debt.

When can the IRS levy?

There are three procedural requirements the IRS must take before they can legally levy:

- The IRS must make a notice and demand for payment

- The taxpayer must refuse or fail to make payment within 10 days of the notice

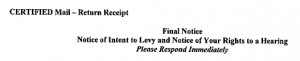

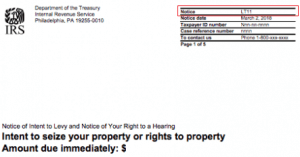

- IRS must give the taxpayer a notice in writing of their 30 day right to hearing before levy is made

The first notice and demand for payment is usually a CP14 notice, which looks like this.

The final notice that provides the taxpayer with a 30 day right to a hearing is a Letter 1058 or LT11.

If you receive either of these letters, you have 30 days to make arrangements with the IRS or request a collections due process hearing.

After those 30 days have lapsed and you have not taken action, the IRS can levy your property, which can be in the form of wage garnishments, bank account levy, and any other personal or business assets.

IRS wage garnishment

Wage garnishments are one the most common types of IRS levy actions.

If the IRS levies (seizes) your wages, part of your wages will be sent to the IRS each pay period.

Part of your wages may be exempt from the levy and the exempt amount will be paid to you. The exempt amount is based on the standard deduction the number of dependents you are allowed for the year the levy is served.

The IRS will leave you with very little income if they garnish your wages. The garnishment will be ongoing until you’ve made arrangements to pay the tax due or if the IRS releases the levy.

IRS bank levy

The IRS can levy any bank accounts that the taxpayer has financial interest in.

Unlike a wage garnishment, an IRS bank levy is not ongoing. Each levy only covers the funds in the account at the time of levy.

If additional deposits are made, the IRS cannot seize them without initiating another levy action.

After your bank receives a levy, it must wait 21 calendar days before surrendering the money to the IRS. This provides the taxpayer an opportunity to notify the IRS of any errors.

During the 21 day period, the taxpayer may not withdraw any funds that were in the account at the time of the levy. The taxpayer may, however, withdraw funds that were deposited after the levy was served.

IRS levy on retirement accounts

It is rare for the IRS to levy retirement accounts. The IRS will only levy such accounts if the taxpayer has engaged in “flagrant conduct” such as:

- Taxpayer’s failure to pay is based on frivolous arguments

- Taxpayer voluntarily contributed to retirement accounts during the time period the taxpayer knew unpaid taxes were accruing

- Taxpayers convicted of tax evasion for the tax debt

- Taxpayers assessed with a fraud penalty for the tax debt

- Taxpayers assisting others in evading tax

- Taxpayers who are in business, pyramiding unpaid trust fund taxes

- Individual taxpayers who are accumulating unpaid income taxes over multiple tax periods and will not adjust their withholding or make timely and adequate estimated tax payments to prevent future delinquencies

- Taxpayers who have demonstrated a pattern of uncooperative or unresponsive behavior that delays the collection of the tax due

- Taxpayers who have placed other assets beyond the reach of the government

Seizure of tangible personal property

In order for the IRS to seize tangible personal property, your case would have to be assigned to a revenue officer. ACS can levy bank accounts and garnish wages, but they will not seize tangible personal property.

Before the IRS can seize tangible property, alternative collection methods, such as an installment agreement, must be thoroughly considered.

Seizure of personal residence

Many taxpayers believe that their personal residence has homestead protection. While that may be true for other creditors, it does not apply to the IRS.

The IRS can levy on a personal residence if a U.S. district court judge approves it in writing and with the approval of the IRS Area Director.

It is very uncommon for the IRS to seize a personal residence.

How to get an IRS levy release

Make arrangements with the IRS

The IRS will release a levy when the taxpayer has made arrangements to pay the debt, such as by entering into a payment plan.

Before the IRS will consider a payment plan, the taxpayer must have filed all tax returns and is paying current taxes.

This could put some taxpayers in a bind if they are not compliant with all their tax return filings. It could take some time before an agreement is reached with the IRS.

The levy causes economic hardship

The IRS must stop the levy action if it causes an economic hardship. A taxpayer has economic hardship if the levy prevents the taxpayer from paying basic living expenses such as food, clothing, shelter, and medical expenses.

A taxpayer does not have to be in compliance on filing and paying current taxes before the levy is released due to economic hardship.

Taxpayer assistance order

If negotiating with the IRS fails, taxpayer can contact Taxpayer Advocate Service (TAS). TAS can stop the levy by issuing a Taxpayer Assistance Order.

TAS should only be contacted in extreme cases after other options have failed.

You should always consult with a tax professional before making any decisions about how to best resolve your particular matter.

Options for resolving tax debt

Taxpayers that owe outstanding IRS tax debt should apply for one of the collections alternatives: